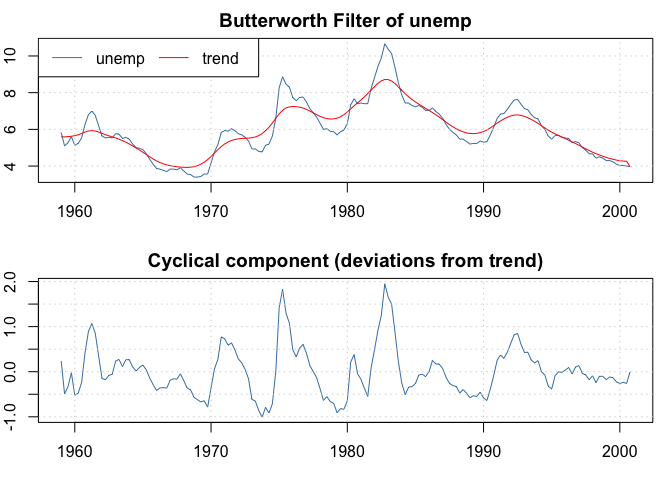

The mFilter package implements several time series filters useful for smoothing and extracting trend and cyclical components of a time series. The routines are commonly used in economics and finance, however they should also be interest to other areas. Currently, Christiano-Fitzgerald, Baxter-King, Hodrick-Prescott, Butterworth, and trigonometric regression filters are included in the package.

You can install the released version of mFilter from CRAN with:

The development version can be installed with:

This is a basic example which shows you how to do Butterworth filtering:

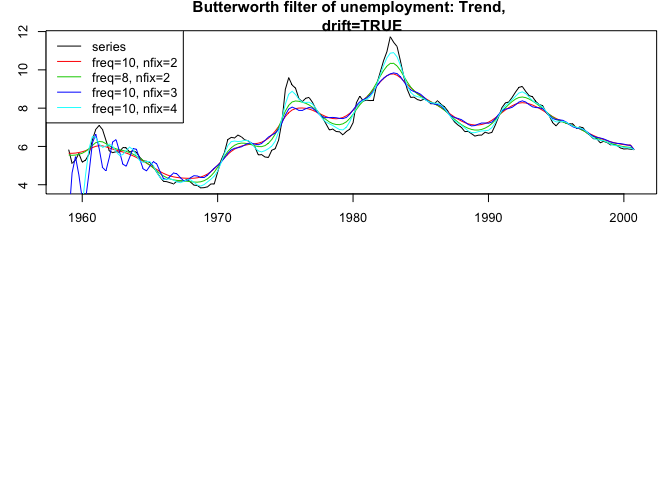

unemp.bw1 <- bwfilter(unemp, drift=TRUE)

unemp.bw2 <- bwfilter(unemp, freq=8,drift=TRUE)

unemp.bw3 <- bwfilter(unemp, freq=10, nfix=3, drift=TRUE)

unemp.bw4 <- bwfilter(unemp, freq=10, nfix=4, drift=TRUE)par(mfrow=c(2,1),mar=c(3,3,2,1),cex=.8)

plot(unemp.bw1$x,

main="Butterworth filter of unemployment: Trend,

drift=TRUE",col=1, ylab="")

lines(unemp.bw1$trend,col=2)

lines(unemp.bw2$trend,col=3)

lines(unemp.bw3$trend,col=4)

lines(unemp.bw4$trend,col=5)

legend("topleft",legend=c("series", "freq=10, nfix=2",

"freq=8, nfix=2", "freq=10, nfix=3", "freq=10, nfix=4"),

col=1:5, lty=rep(1,5), ncol=1)

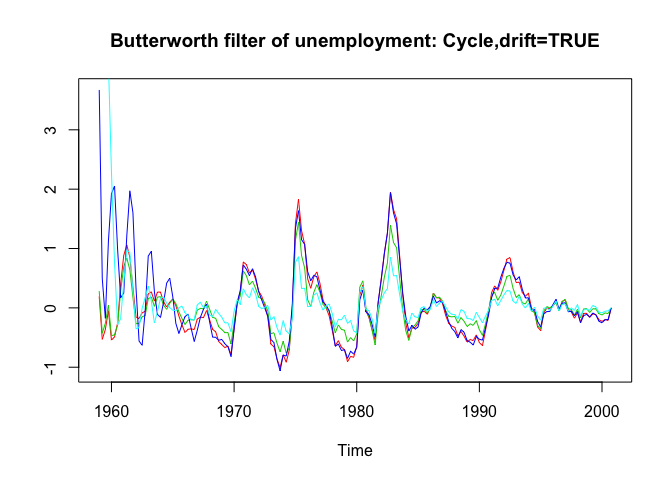

plot(unemp.bw1$cycle,

main="Butterworth filter of unemployment: Cycle,drift=TRUE",

col=2, ylab="", ylim=range(unemp.bw3$cycle,na.rm=TRUE))

lines(unemp.bw2$cycle,col=3)

lines(unemp.bw3$cycle,col=4)

lines(unemp.bw4$cycle,col=5)